Impact of United States Policies on the Indonesian Economy (2020-2023)

Meita Rosa Indah – IES Nurjihan Khairunisa – IES

The world has experienced a series of crises, from endogenous to exogenous shocks. Endogenous crises such as the global financial crisis (2008-2009) caused by the actions of market participants, bankers, and speculators. Meanwhile, exogenous crises were specified by factors outside the economy, such as health issues exemplified by the COVID-19 pandemic.

The COVID-19 pandemic had a peculiar impact which represented a twin shock of both demand and supply sides. The coronavirus disease was first detected in December 2019 in Wuhan, China, and it spread worldwide, becoming a pandemic on March 11, 2020. Social restrictions were implemented to curb the virus’s spread, disrupting economic activities from store closures to mass layoffs, ultimately leading to economic weakening.

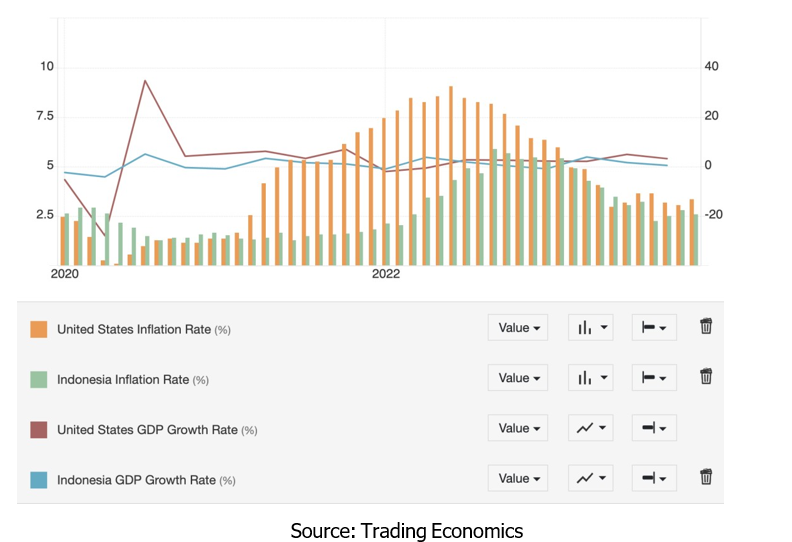

This economic weakening spared no one, not even superpowers like the United States. The US economy recorded negative growth in Ǫ1 2020 at -5.3%, followed by a -28% decline in Ǫ2 2020, resulting in the highest inflation rate in four decades. Indonesia, as a developing country with close ties to advanced economies, it was also affected by these crises. However, the extent of the impact and the transmission mechanisms to Indonesia need further examination.

This article will analyze and answer the hypotheses: (1) The United States economy affects the Indonesian economy through the transmission of economic fundamentals, (2) The United States economy affects the Indonesian economy through financial market transmission, (3) The United States economy affects the Indonesian economy through the transmission of US policy responses.

Period of Expansive Fiscal and Monetary Policies

The COVID-19 pandemic brought the US economy to extremely drop in the first year to shrink -5.3% (ǪoǪ) in Ǫ1 2020, followed by a decline of -28% (ǪoǪ) in Ǫ2 2020, marking the largest quarterly drop. The economic growth contraction occurred due to lower demand for goods and services as indicated by US Inflation in March 2020 of 1.5% (YoY), the lowest in 14 years. Unemployment in the US also surged from 3.5% in February 2020 to 14.7% in April 2020.

The rapid spread of the coronavirus sparked investor concern and disrupted global supply chains. In March, the S&P 500, one of the major stock indices in the US, experienced its worst decline since 1987, plummeting about 20%. The 10-year Treasury yield also hit a record low below 0.6%. The US trade deficit in 2020 reached -$685.5 billion, up 107% (YoY) compared to the previous year.

The US government and The Fed (US Central Bank) established policies to prevent catastrophic pandemic impacts. The US government provided a fiscal stimulus known as the CARES ACT, amounting to $2.2 trillion in response to the pandemic. On the monetary side, The Fed lowered interest rates to 0%-0.25% in March 2020 to prevent credit defaults

and conducted Ǫuantitative Easing (ǪE) by purchasing US Treasuries worth USD 80 billion and Mortgage-Backed Securities (MBS) worth USD 40 billion monthly.

Similarly, Indonesia was hit hard by the pandemic. COVID-19 was first detected in Indonesia on March 2, 2020, but economic slowdown had already begun. Indonesia’s GDP slowed in Ǫ1 2020 to -2.41% (ǪoǪ) and continued in Ǫ2 2020 at -4.19% (ǪoǪ). This slowdown occurred due to global supply chain disruptions, especially from China, decreased consumption, and the implementation of social restrictions contributing to the economic downturn in the second quarter. By sector, there was a decline in food and beverage accommodation services by -22.02%, transportation and warehousing by – 30.84%, and trade by -7.57%.

A slowing purchasing power indicator can also be seen from the anomaly of inflation into Ramadan (April 2020). Inflation, which usually rises before Ramadan, declined this year. The annual core inflation component (YoY), indicating demand-supply interaction, consecutively fell to 2.85%; 2.65%; and 2.26% from April to June 2020. The annual inflation (YoY) for volatile foods decreased and stabilized around two percent, indicating stable food production. Furthermore, the administered price inflation component on an annual basis (YoY) in April-June 2020, amounted to -0.09; 0.28; and 0.52 percent respectively. Deflation in administered price component in early Ǫ2 2020 was driven by a decrease in transportation sector activity due to social restrictions. Thus, low inflation in 2020 is defined as economic sluggishness, where businesses struggled to raise prices due to weak consumer demand.

The economic downturn resulted in an increased of open unemployment rate in Indonesia, from 4.94% in February 2020 to 7.07% in August 2020. The tourism sector was most affected, followed by declines in hotels, restaurants, and airlines. The pandemic’s impact targeted labor-intensive sectors due to activity restrictions under large-scale social restrictions (PSBB).

Indonesia’s financial and commodities markets were also affected by the pandemic. As COVID-19 was confirmed in Indonesia, the Jakarta Composite Index (IHSG) fell to its lowest level at 3,937.6 in March 2020. This decline caused Indonesia’s market capitalization to plummet to Rp4,556.3 trillion or a decrease of more than Rp2,690 trillion from early 2020. Government Securities (SBN) yields fluctuated in line with global market developments. High volatility occurred from March to May 2020, causing the 10-year SBN yield to rise significantly to 8.38% (+135 bps) on March 24, 2020, compared to the January 3, 2020, yield

of 7.03%.

The government and Bank Indonesia (BI) implemented policies to safeguard the economy. Fiscal stimulus was applied in the form of tax relaxation1, export-import support2, and increased government spending on health, social safety nets, and business industries. The relocation of state spending to these sectors reached Rp405.1 trillion. On the monetary side, BI lowered its benchmark interest rate (BI7DRR) by 75bps in 2020 to 3.75% and conducted quantitative easing. BI lowered the Rupiah Reserve Requirement (GWM) by 200bps for conventional commercial banks and 50bps for Sharia commercial banks/Sharia Business Units. In addition, BI purchased government securities with a total value of Rp601.7 trillion, reflecting 53.8% of the total issuance of tradable government securities in 2020. This policy was regulated under the Joint Decree of the Minister of Finance and the Governor of Bank Indonesia No. 347/KMK.08/2020 and 22/9/KEP.GBI/2020 dated July 20, 2020. The Financial Services Authority (OJK) also intervened to protect investors from extreme fluctuations in share prices through changes in Auto Rejection Limits. Auto Reject Bawah (ARB) is an automatic rejection that occurs when a stock price drops significantly, causing the system to automatically reject buy orders or limit the number of shares that can be sold at a certain price. If a stock drops by 10%, it will automatically be rejected. This decision was made considering the concerning condition of the capital market.

The provision of stimulus pushed the recovery of Indonesia’s economic growth in the third quarter of 2020. Indonesia’s GDP grew positively in Ǫ3 2020, reaching 5.05% (ǪoǪ). However, consumer purchasing power remained low, reflected in the declining core inflation trend. Annual inflation in 2020 was 1.68% (YoY), the lowest recorded inflation in Indonesia’s history. Indonesia’s trade balance surplus for 2020 amounted to $28.30 billion, driven by non-oil and gas surpluses, primarily palm oil exports and precious metals, and a low oil and gas deficit due to decreased fuel consumption during the pandemic. However, there was an increase in imports for health equipment, including masks, rapid tests, PCR tests, vaccines, etc. But overall, export-import activities remained in negative zone.

1 The government will bear 100% of Article 21 Income Tax for employees with incomes up to IDR 200 million in the manufacturing sector; relaxation of Article 22 Import Tax; relaxation of Article 25 Income Tax; and

relaxation of VAT restitution.

2 Simplification and reduction of the number of prohibitions and restrictions on export and import activities, especially for raw materials; acceleration of export and import processes.

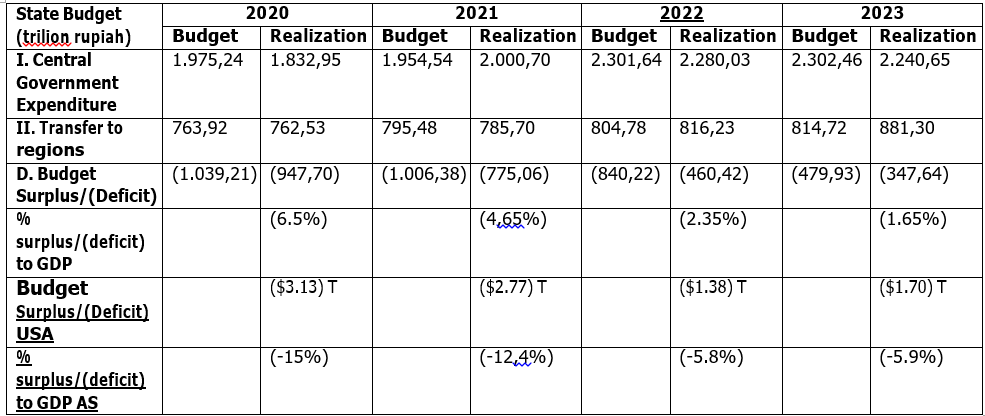

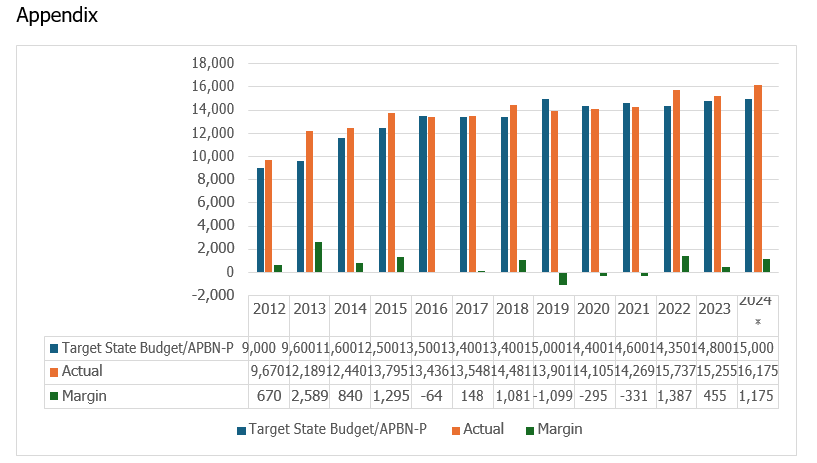

The increase in state spending to stimulate and address the pandemic has led to a 2020 budget deficit of Rp947.70 trillion (6.14% of GDP in 2020). This exceeds the upper limit of the budget deficit based on the State Budget Law under normal conditions, which should be 3% of GDP. The increases in the expenditure realization are mainly due to government programs in supporting the National Economic Recovery (PEN) program to respond to the impact of the Covid-19 pandemic, such as payments for MSME assistance, wage subsidies, incentives for health workers, reimbursement of referral hospital claims, and procurement of health equipment and/or infrastructure in the handling Covid-19.

The policies implemented by the government and Bank Indonesia were quite effective. These policies prevented a more severe economic downturn, with economic growth recovering in the third quarter of 2020. Inflation was at a low but controlled level of 1.68% (YoY). As well as a decline in the unemployment rate which was reflected in February 2021 at 6.26% YoY (-0.81% compared to August 2021 TPT). The stock market did show weakness and recorded negative growth but the regulation from OJK can dampen the impact more severely.

Impact of U.S. Fiscal Stimulus on Indonesia (2020-2021)

The U.S. fiscal stimulus in 2020-2021 impacted Indonesia’s trade balance. The stimulus successfully stimulated domestic economic growth and increased consumer purchasing power in the U.S., leading to higher demand for goods and services, including imported goods from Indonesia. Considering that the United States is Indonesia’s second-largest

trading partner after China, towards the end of 2020, there was an increase in non-oil and gas export performance. The main commodities exported to the U.S. were articles of apparel and clothing accessories (HS Code 61) with a value of USD 1.89 billion. U.S. export value in 2020 was recorded at USD 1.81 billion, up from the previous period’s USD 1.11 billion. In 2021, export performance also improved, with Indonesia’s exports to the U.S. increasing by 38.40% (YoY) and accounting for 11.75% of Indonesia’s total non-oil and gas exports in 2021. These exports were valued at USD 25.8 billion, with the highest commodity values being articles of apparel (HS 61) and rubber (HS 40).

Impact of U.S. Ǫuantitative Easing on Indonesia

The Fed implemented Ǫuantitative Easing (ǪE) policies by purchasing USD 80 billion in government bonds and USD 40 billion in Mortgage-Backed Securities (MBS) to stimulate the economy. During the period of Ǫuantitative Easing by The Fed, banks in the United States received significant capital injections. Much of this capital was used to invest in emerging markets, including Indonesia. Investment activities due to the Ǫuantitative Easing policy led to capital inflows into Indonesia. In 2020, capital inflows reached USD 912 million and USD 1.7 billion in 2021, higher than in 2019, which was only USD 374 million.

Economic Conditions in the US and Indonesia in 2021

The rapid vaccination rollout, continuation of fiscal stimulus, and monetary policy easing from the previous year droved the U.S. economic recovery in 2021. U.S. GDP grew by 5.8% (YoY); however, the U.S. trade deficit persisted and increased to $948.1 billion in 2021, the highest since 2008. Additionally, a significant rise in inflation triggered global concerns about the impact of the Fed’s tightening monetary policy.

Fiscal and monetary policy harmonization continues to support Indonesia’s economic recovery from the impact of the Pandemic. The Indonesian government allocated a budget for the National Economic Recovery (PEN) Program amounting to IDR 744.77 trillion in 2021. On the monetary side, Bank Indonesia continued purchasing Government Securities (SBN) to fund the 2021 State Budget (APBN) amounting to IDR 358.32 trillion3 and lowered the interest rate to stimulate domestic economic activity. The benchmark interest rate (BI7DRR) was cut by 25 basis points to 3.50% in February 2021 and maintained throughout the year. Policy mix was also implemented through the Financial System Stability Committee (KSSK) to encourage the reduction of banking credit interest rates and credit restructuring.

3 (i) Purchases in the primary market amounting to IDR 143.32 trillion in accordance with the Joint Decision of the Minister of Finance and the Governor of Bank Indonesia, valid until December 31, 2022, and (ii) private placement amounting to IDR 215 trillion for financing healthcare and humanitarian efforts.

Indonesia’s economic growth in 2021 showed improvement despite a contraction in the third quarter of 2021. Economic growth performance continued to increase, reaching 7.07% in the second quarter of 2020, driven by export activities (+29.83% YoY) and imports (+23.31% YoY). However, growth was slightly hindered by the surge of the Delta variant in July-August 2021, resulting in economic growth at 3.51% (YoY) in the third quarter of 2021. In the fourth quarter of 2021, economic performance improved, growing by 5.02% (YoY), indicating a strengthening economic recovery, even higher than the fourth quarter of 2019 (pre-pandemic) growth of 4.96% (YoY).

The 2021 PPKM policy due to the Delta variant led to a decline in economic activity, impacting the decline in consumer purchasing power. National inflation in 2021 remained low at 1.87% (YoY) in line with still-weak demand and adequate supply. This inflation was below the 2021 State Budget assumption of 3.0% (YoY). Annual inflation increased, but there was a monthly deflation of 0.16% (MoM) in June 2021. Generally, low national inflation was influenced by the stability of all inflation components, including core inflation at 1.56% (YoY); administered price inflation at 1.79% (YoY); and volatile food inflation at 3.20% (YoY).

Uncertainty in the financial market4 affects the liquidity of global and domestic financial markets. Throughout 2021, the 10-year SBN interest rate has quite high volatility in line with financial market uncertainty, the surge in Covid-19 cases in almost all countries, and a wait-and-see attitude from foreign investors towards entering emerging markets. The highest spike in SBN yields occurred in the first quarter of 2021, reaching 6.80% in March 2021. In addition, financial market uncertainty resulted in a decrease in incoming bids in SBN auctions. The Jakarta Composite Index (JCI) recorded an upward trend from January to December 2021. After rising early in the year to 6,435.21 points on January 13, 2021, the JCI experienced a downward trend, hitting its lowest level on May 19, 2021, at 5,760.58 points, and then began to rebound until the end of December 2021, closing 0.29% or 19.20 points at 6,581.48.

The increase in the Indonesian Crude Price (ICP) in 2021 determines the structure of the State Budget (APBN). The average Indonesian crude oil price in 2021 increased to

$68.47/Barrel, higher than the ICP in 2020 of $40.39/Barrel. This increase affected Non-Tax State Revenue (PNBP), particularly revenue from crude oil, as well as Income Tax on Oil and Gas (PPh Migas). This increase contributed Rp27.54 trillion or equivalent to 52.69% of the total increase in PNBP from natural resources. On the expenditure side, ICP influenced energy subsidy spending and revenue-sharing funds (DBH) to regions. Indonesia’s energy

4The increase in United States Treasury (UST) yields, which has driven up global interest rates, uncertainty over tapering policies in the USA and Europe, and a surge in debt in nearly all countries due to the high financing needs of COVID-19, have all contributed to the rise in refinancing risk.

subsidies in 2021 amounted to Rp140.41 trillion, an increase of 28.95% compared to the same period the previous year.

Throughout 2021, Indonesia’s export value experienced a decent development with a increasing growth rate. Positive export growth is coupled with increasing imports as production activities and domestic demand begin to improve. The positive export performance outpaced import performance, resulting in a trade balance surplus of $35.33 billion in 2021.

Government policies succeeded in boosting Indonesia’s economic growth in 2021. Indonesia experienced GDP growth of 3.69% (YoY) throughout 2021, higher than in 2020, which had experienced a contraction. The unemployment rate was recorded at 6.49% in August 2021, down 0.58% compared to August 2020. However, this recovery has not been able to increase purchasing power as seen by the low inflation.

Fiscal Policy Normalization and Contractionary Monetary Policy Period Impact of US Tapering Off on Indonesia (Nov 2021-2023)

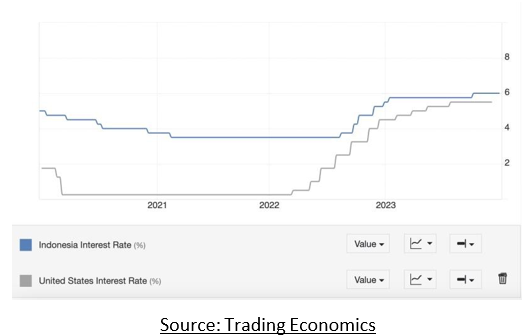

The massive increase in US inflation prompted the Fed to aggressively normalize its monetary policy in 2021. The Fed began reducing its liquidity injections (tapering-off/TO) in the financial market from US$120 billion to US$15 billion per November 2021. Unlike previous instances, this tapering-off could be mitigated as it was anticipated.

The destructive impact of tapering off was not as strong as before because Indonesia’s foreign exchange reserves were quite high, amounting to US$146.9 billion, equivalent to financing 8.0 months of imports or 7.8 months of imports and government external debt payments. Large foreign exchange reserves can act as a buffer through exchange rate stabilization policies during tapering periods. The reserves can be used to meet domestic US dollar needs. Additionally, the ratio of foreign ownership in SBN was only around 19.0 percent, which limited capital flight during tapering, and the national banking industry currently has strong and stable fundamentals. On November 4, 2021, when tapering was announced, the rupiah immediately dropped by 0.37% to Rp14,366 per dollar but stabilized after 5 working days. This tapering prompted Indonesia to increase retail investor participation in SBN.

Economic Conditions in 2022

The high inflation felt by the US has led the Fed to tighten monetary policy through faster and more aggressive FFR hikes. Inflation in June 2022 reached 9.1% (YoY), the highest in the last 40 years. Geopolitical tensions, with Russia and Ukraine being major exporters of energy and wheat, led to rising energy and food Geopolitical tensions between Russia and

Ukraine, which are major energy and wheat exporters, resulted in higher energy and food commodity prices. These commodities contribute to US food and energy inflation. Not surprisingly, inflation in America in June 2022 in detail; General: 5.9% (YoY), Food: 10.4% (YoY), and Energy: 41.6% (YoY).

Indonesia experienced a significant increase in inflation in 2022, reaching 5.51% (YoY), as all inflation components rose. Disaggregation of this inflation consists of core inflation at 3.36% (YoY), administrate price components at 13.34% (YoY), and volatile component inflation at 5.61% (YoY). The increase in core inflation was driven by the recovery of purchasing power and domestic demand, transmission of global commodity inflation to the domestic market, and depreciation of the rupiah exchange rate. On the other hand, the increase in government-regulated price components was influenced by adjustments in fuel prices5 and the rise in non-subsidized energy commodity prices such as Liquefied Petroleum Gas (LPG) 12kg. Meanwhile, the increase in volatile component inflation was influenced by weather anomalies that led to crop failures and rising global food prices that affected domestic commodities.

Indonesia’s economy grew strongly in 2022, reaching 5.3% (YoY). The highest growth occurred in the Export of Goods and Services component at 16.3% (YoY), which was a windfall from the increase in prices of Indonesia’s leading commodities in the global market such as coal, iron ore, and palm oil. The recovery of investment/Gross Fixed Capital Formation (GFCF) continued in 2022, with high demand for downstream products driving investment activities. This is evidenced by investment in machinery and vehicles growing by 22.4% and 10.3% respectively (YoY).

Indonesia’s trade surplus in January-December 2022 amounted to $54.46 billion. The export surplus was influenced by the rise in global commodity prices along with geopolitical tensions between Russia and Ukraine, while Indonesia’s imports showed an increase in line with the rapidly recovering domestic economic activity. Indonesia’s export value in 2022 reached $291.98 billion (+26.07% YoY), while imports reached $237.45 billion (+21.03% YoY).

The financial market conditions in 2022 were quite conducive. The Indonesian stock market in 2022 closed 4.09% (Ytd) at the level of 6,850.52. At the opening, the Jakarta Composite Index (IHSG) was at 6,665.31, then moved dynamically and reached its highest point on September 13, 2022, at 7,318.02. Increased global uncertainty 6caused pressure on

5 The government has increased the prices of Pertalite type of gasoline by 30.72%, Solar by 32.04%, and Pertamax by 16%.

6 Amid ongoing geopolitical conflicts, rising commodity prices, increasing Fed benchmark interest rates, and global liquidity tightening,

the IHSG, which closed at 6,850.62 at the end of 2022. The bond market was also favorable, with SBN yields still below the APBN target but increasing in the second to fourth quarters, reaching 7.61% in October 2022. Global uncertainty was the cause of the rise in SBN yields. Support from Bank Indonesia through SKB I (standby buyer) and SKB III (burden sharing in the issuance of SBN in the health and humanitarian fields) helped maintain bond yield.

The vaccination program and the continuity of the National Economic Recovery Program (PEN) have successfully boosted public and market confidence, thereby increasing national economic activity. PEN has contributed to a decrease in the Open Unemployment Rate (TPT) in August 2022 to 5.86% (-0.63% YoY). The number of working-age population affected by Covid-19 was recorded at 4.15 million people, a decrease of 17.17 million people from August 2021.

At the end of 2022, the rupiah exchange rate against the US dollar depreciated to Rp15,592/USD (-9.31% YoY) compared to the last trade in 2021, which was Rp14,263/USD. This depreciation was driven by the Fed’s interest rate hike and global uncertainty. The rising US interest rates prompted investors to switch and hold their money in the US as it was perceived to offer higher returns with lower risks. Ultimately, this led to a decrease in the supply of US dollars in Indonesia due to capital outflows, resulting in depreciation.

Bank Indonesia intervened to address rupiah pressures and started normalizing policies. Bank Indonesia raised the BI7DRR to 5.5% (+200 bps) in the second half of 2022 from 3.5% in July 2022. Liquidity tightening was also implemented by gradually increasing the Minimum Reserve Requirement (GWM) from 3.5% to 9.0%. These policies succeeded in mitigating the depreciation pressure on the rupiah in the fourth quarter of 2022. On average, the exchange rate of the rupiah in 2022 depreciated by 3.9% compared to 2021, from Rp14,312/USD to Rp14,871/USD, but performed better than other emerging countries such as India, Thailand, and Malaysia.

The impact of the increase in the Fed Funds Rate (FFR) in Indonesia

Since March 2022, the Fed has raised its interest rates by 525 basis points to 5.50%. As of April 2024, the interest rate has been maintained at a high level (5.50%) given that the inflation target has not been achieved. Meanwhile, the increase in interest rates began in

Bank Indonesia in August 2022 due to inflation exceeding the target range of 3±1% in the previous month and the further depreciation of the rupiah. The increase has reached up to 5.75% by January 2023 and was maintained until the beginning of Ǫ4 2023. Then, it was raised again by 25 bps to 6%, and it is predicted to be maintained until the second half of 2024.

The narrowing gap/spread between the Fed Funds Rate and BI-7DRRR has resulted in capital outflows. As of January 2024, the difference between these two interest rates is only 0.5%. Analogically, if Indonesia is rated BBB while the US is at AAA, investors will automatically shift their investments to AAA-rated countries for higher returns with lower risks.

The impact can be seen in the weakening of the rupiah exchange rate and the Jakarta Composite Index (JCI). When the Fed raises its interest rates, the US dollar becomes more attractive to foreign investors, leading to the appreciation of the dollar and the depreciation of the rupiah. As seen in graph, the rupiah exchange rate has now breached the level of Rp15,600 per US Dollar due to the high pressure resulting from the increase in the Fed’s interest rates. Sentiments from the US economy also affect stock trading in Indonesia. When the issue of the Fed’s interest rate hike occurred, it negatively affects investors in Indonesia. This series of events caused a negative trend from April 2022 to May 2023 which resulted in Indonesian stocks being corrected.

Condition in 2023

Monetary tightening, geopolitical tensions (Ukraine-Russia and Palestine-Israel), and climate change factors haunted the economic recovery. Throughout 2023, the Fed raised interest rates at 4 meetings and maintained rates at 4 other meetings, remaining at 5.5% by December 2023. Geopolitical tensions also caused the US debt ceiling (US$31.4 trillion) to

be breached due to foreign aid demands and security spending. Climate change also disrupted food supply and production, leading to inflation. 2023 was recorded as the hottest year in history driven by the El Niño weather phenomenon.

The failure of major banks such as Silicon Valley Bank and Signature Bank characterized the US financial market turmoil. The collapse of these banks was caused by the unexpected increase in the FFR, overly risky long-term investment decisions, and massive withdrawals by customers. Other banks like Silvergate and Signature Bank, focusing on the cryptocurrency and blockchain industries, also experienced crises and collapsed due to instability in the stable coin market.

Amid economic challenges and global uncertainty, Indonesia’s economic growth remained resilient. Indonesia’s GDP reached 5.05% (YoY) driven by a 39.13% increase in government consumption, followed by the PK-LNPRT component at 11.75%. On a quarterly basis, Indonesia’s economy in 2023 grew above 5% in the first to third quarters. Indonesia’s inflation achievement in 2023 remained stable and controlled within the target range of 3%±1%. The inflation achievement for 2023 was recorded at 2.61% (YoY), a decrease compared to the realization in 2022, which was 5.51% (YoY).

Indonesia’s trade balance in 2023 recorded a surplus of USD36.93 billion. Indonesia’s export value reached $258.82 billion, experiencing a decrease in value from the previous year due to the moderation of prices of main commodities such as palm oil and coal. However, in terms of volume, Indonesia’s exports in 2023 still grew positively at 8.55% (YoY). Meanwhile, Indonesia’s imports reached $221.89 billion (-6.55% YoY) due to the largest slowdown in imports being machinery or electrical equipment and their parts, while machinery and mechanical equipment and their parts contributed to the increase in imports. Similarly to exports, in terms of volume, Indonesia’s imports still recorded positive growth at 8.04% (YoY), in line with the continued strength of domestic demand.

The performance of the Indonesian financial market in 2023 ended on a positive note. The Jakarta Composite Index (IHSG) in 2023 closed with a gain of 6.16% (Ytd) at the level of 7,272.79, higher than the achievement in 2022 which was 4.09% (Ytd). IHSG experienced volatility in the first two quarters as investors were made pessimistic by the International Monetary Fund (IMF) projections, forecasting that one-third of the world’s economy would fall into recession, China’s economic slowdown which would have a negative impact, and the Federal Reserve’s “higher for longer” interest rate stance. However, positive domestic sentiment through large dividend distributions and solid economic data releases strengthened the IHSG. Even the market capitalization value reached Rp11,762 trillion on December 28, 2023 (+22.9% YoY).

On the bond market side, there was an increase in demand for long-term tenor bonds, reflected in the average decrease in yields for long-term tenors (>7 years) by up to – 42.73bps (YoY). Meanwhile, medium-term SBNs (5-7 years) experienced an average yield decrease of -19.19bps (YoY). Market participants took advantage of the potential for capital gains on long-term tenors in line with expectations of economic slowdown and inflation in the future.

Aligned with economic recovery and the easing of COVID, the Indonesian government normalized its policies. On the fiscal side, there was tax normalization for state revenues regulated in the Harmonization of Tax Regulation Law (UU HPP) and optimization of Non-Tax State Revenue (PNBP). State revenue realization reached Rp2,774.3 trillion (+5.3% from 2022 realization) while state expenditure realization reached Rp3,121.9 trillion (+0.8% from 2022 realization). On the monetary side, Bank Indonesia maintained a high BI-Rate of 6.00% to strengthen the stabilization of the rupiah exchange rate and ensure inflation remained under control within the target range. Interventions in the forex market in spot transactions, Domestic Non-Deliverable Forward (DNDF), and Government Securities (SBNs) in the secondary market were carried out to maintain rupiah stability. The Financial Services Authority also normalized stock market policies through adjustments to the percentage limits of Auto Rejection Bottom.

Banking crisis in the US and its impact on Indonesia

The impact of the US bank run is a lesson learned but does not have much impact on Indonesia. Unlike SVB and banks in the US, banks in Indonesia do not provide credit and investment to startup technology companies or cryptocurrencies, and the resilience of the Indonesian economy remains intact. This has a positive impact on Indonesia, as the price of certified Antam gold bars, PT Aneka Tambang (ANTM), rose by Rp 6,000 per gram. From the previous Rp 1,072,000 per gram, the current price of gold is Rp 1,078,000 per gram, and government bonds as of March 2023 are in demand, resulting in a decrease in yields to 6.815 (-1.2% MoM).

The US banking crisis also provides lessons for regulators and financial services in Indonesia. Mahendra Siregar, Commissioner of the Financial Services Authority (OJK), stated that fundamental asset-liability risk management had been violated, and excessive sector concentration was the cause of the crisis. On the other hand, there was a mismatch in short-term deposits, where banks placed them in medium-to-long-term government bonds. Additionally, the rapid increase in the FFR, which was not anticipated by SVB, is evident in the placement of bonds for hold-to-maturity at $89 million USD compared to available-for-sale bonds of around $28 million USD, as per the December 2022 financial report.

Conclusion:

The fundamentals of the US economy do not significantly impact the Indonesian economy. During the COVID-19 pandemic, economic growth and inflation between the United States and Indonesia did not move in the same direction due to domestic influences. In 2021, while inflation increased in the US, Indonesia experienced a decrease due to the balance of supply and demand of domestic rice prices as rice was abundant.

The US financial market transmission had a moderate impact on the Indonesian financial market through investor sentiment and perception. In the capital market, negative sentiment in the US directly resulted in a decline in the JCI. The Financial Services Authority’s micro prudential policies were successful in preventing more severe fluctuations in the stock market by maintaining upper and lower limits on stock trading. Meanwhile, the increase in bond yields in the United States reduced investor interest in Indonesian bonds, leading to a decline in bond prices. Bank Indonesia purchased government bonds in the primary and secondary markets to support the stability of SBN market prices, thereby supporting sustainable fiscal financing and assisting in financing pandemic mitigation efforts.

The policy response from the United States has a significant impact on the Indonesian economy, especially monetary policy. US fiscal expansion policies led to increased demand for imports of goods and services from Indonesia, thus driving Indonesia’s trade surplus. Meanwhile, US monetary policy has a significant impact on the Indonesian economy, particularly on the exchange rate of the rupiah. The increase in US interest rates makes the US dollar more attractive due to the higher yields, causing investors to withdraw their funds (capital outflow) from Indonesia and triggering depreciation of the rupiah.

Indonesia’s fiscal and monetary policies are considered effective in addressing the pandemic and global challenges, although there are some notes. Expansive fiscal policies have driven domestic demand recovery, economic growth, and trade surplus. Meanwhile, expansive monetary policy has helped boost the economy through banking credit relaxation and burden-sharing schemes. From 2022 to 2023, fiscal policy normalization has brought the budget deficit back below 3% of GDP. Monetary policy contraction through interest rate increases since August 2022 has helped curb the depreciation of the rupiah exchange rate. However, Bank Indonesia is tasked with maintaining rupiah exchange rate stability amid the “higher for longer” US interest rate policy, predicted to be maintained until the end of 2024. Regulations from the Financial Services Authority also help prevent stock market crashes through auto rejection rules.

Policy Recommendations:

Policy interventions are crucial, with speed and accuracy being the key factors to success. Therefore, policymakers must act promptly and achieve the set intervention targets. Moreover, the policies implemented should be based on the potential and opportunities available for Indonesia in the future.

- A burden-sharing scheme between the Government and Bank Indonesia (BI) is both appropriate and essential to assist the country in addressing the economic crisis caused by the COVID-19 With this scheme, the government can reduce fiscal burdens and allocate more funds to priority programs such as healthcare, social assistance, and support for MSME during times of crisis.

- The policy of increasing interest rates in 2022-2023 succeeded in reducing the depreciation of the rupiah exchange rate triggered by expectations, although the exchange rate remained above the target level from 2022 to May 2024. The ongoing depreciation raises questions about the effectiveness of this monetary policy in controlling market

- Indonesia should reconsider its policy of product diversification and differentiation of trading partner countries given that its largest trading transactions are with China and the United However, Indonesia also needs to expand its trade relations with other potential partner countries, such as Nigeria, which is projected to experience a demographic bonus by 2050.

Leave a Reply