The covid pandemic from 2019 to 2021 affects banking profitability, especially in 2020. This is shown by the performance of Return On Asset (ROA) KBMI-1 which decreased by 1.55% from 1.17% (2019) to -0.38% (2020). Profitability is one of the most important performance indicators for banks. Profitability shows the bank’s ability to generate profit from its assets. The higher the bank’s profitability, the better the bank’s performance. Nguyen (2020) found that capital adequacy, net interest margin, and non-interest income have a positive effect on profitability, while non-performing loans have a negative effect on bank profitability. If there is an increase in non-performing loans, banks need to increase the allocated reserves. Allowance for impairment losses (CKPN) is a reserve established by banks to anticipate losses due to impairment of their financial assets, such as loans, securities, or other assets and to increase customer confidence.

The following analysis focuses on KBMI-1 and 2 banks of KBMI-1 with data from January 2016 to June 2023, as they are suspected to have structural problems. The hypothesis used in this analysis is that there is a positive correlation between profitability and capital adequacy level (CAR), credit management strategy, and interest rate setting strategy.

Correlation between Capital Adequacy and Profitability

Bank capital adequacy refers to the availability of funds owned by the bank in connection with the overall risk and future expansion. Capital serves as a shield to absorb potential losses and ensure the stability of the bank’s financial position. OJK sets the minimum capital requirement or CAR of banks at 8%, to maintain the stability of the financial system and protect the interests of depositors, shareholders and other parties involved. With sufficient capital, banks can increase stakeholder confidence, being able to bear risks when banks provide credit without compromising the financial stability of the bank. Furthermore, banks that have sufficient capital can reduce the risk of losing the trust of financial markets and the public so that the cost of bank funding can be cheaper.

To fulfil capital adequacy while strengthening the banking industry and improving the economy, OJK issued provisions for commercial banks to adjust their minimum core capital. According to POJK Number 12/POJK.03/2020 regarding the Consolidation of Commercial Banks, there are groupings of Banks based on core capital, namely Bank Groups Based on Core Capital (KBMI-1 to KBMI-4), must meet a minimum core capital of Rp. 1 Trillion by 31 December 2020, Rp. 2 Trillion by 31 December 2021 and Rp. 3 Trillion by 31 December 2022. When a bank’s core capital is strong enough along with adequate risk controls, it can support an increase in CAR and provide the bank with protection against potential losses. With adequate CAR, banks can be more flexible in providing credit, managing investment risk, and maintaining financial stability.

Factors that affect CAR such as: credit risk, asset quality, capital efficiency, investor confidence and credit management. Good credit management contributes to an increase in a bank’s CAR. The benefits of good credit risk management can strengthen the bank’s capital position and support sustainable growth. In general, the CAR of KBMI-1 since 2017 has tended to increase from 22.97% (2018) to 30.93% in 2022. Similarly, bank A which was at 18.11% in 2020 then rose to 53.77% in 2022, and bank B which was generally in the range of 11.59% in 2020 to 14.88% in 2022. The data shows that despite the pandemic, banks in KBMI-1 are still able to maintain a minimum CAR level of 8%.

The statistical test results with a significance level of 5% show that the CAR of KBMI-1 has a significant value of 0.359 while bank A has a significant value of 0.042 and bank B has a significant value of 0.064 so that the test results show there is no significant correlation between the level of capital adequacy (CAR) with the level of bank profitability. This is due to OJK’s requirement for KBMI-1 to adjust the minimum core capital at the end of the period, namely IDR 1 trillion at the end of December 2020, IDR 2 trillion at the end of December 2021 and IDR 3 trillion at the end of December 2022 so that the bank’s CAR does not decrease.

Correlation between credit management strategy and profitability

The main objective of a credit management strategy is to minimise credit risk, maximise returns, and maintain the financial health of the bank. This strategy involves policies and procedures implemented to assess, monitor, and manage the risks associated with lending. Overall, credit management strategy is an important pillar in achieving sustainable bank profitability. One indicator of the success of credit management is by looking at the extent to which KBMI-1 maintains Non Performing Loan (NPL).

In general, since 2018 the NPLs of KBMI-1 as well as bank A and bank B are below 5%, even bank A can maintain its NPLs from 2020 to 2022 at 0.00%. That shows bank A can manage its credit well. The increase was only in KBMI-1 in 2019 which rose from 2.77% to 3.69% in 2020. In 2021 the KBMI-1 NPL rate fell again at 2.78%. The statistical test result of KBMI-1 with a significance level of 5%, shows a significant value of 0.624 while bank A with a significant value of 0.000 and bank B with a significant value of 0.119. The results of this statistical test indicate that NPLs in general do not have a significant correlation with ROA, so it can be concluded that there is no significant correlation between credit management strategies and the level of bank profitability. This is because NPLs did not surge with the government’s restructuring programme in 2020 to control bad loans due to the pandemic. The restructuring programme managed to keep NPLs from soaring and banks were able to improve the condition of customers who were still able to survive and return to normal operations.

Internally, the KBMI-1 banks took various steps to improve credit quality. In bank A, with good credit management and low NPL level, bank A can overcome the problem of declining assets, deposits and credit growth through market segmentation, maintaining credit quality so that it can grow 50%. Bank B, with strict credit restructuring management, maintaining liquidity and good credit risk management, can significantly increase credit growth and increase profits. The bank’s credit management strategy is closely related to the determination of interest rates and both influence each other in the context of banking finance, because reasonable interest rates can encourage healthy credit growth.

The correlation between interest rate setting strategy and profitability

An interest rate setting strategy is a plan or approach used by banks to set interest rates on the financial products they offer, especially loans and deposits. The main objectives of this strategy are to optimise the bank’s interest rate income, manage risk, and increase profitability through appropriate interest rate adjustments. The strategy involves several components namely market analysis, risk evaluation, product interest rate setting and economic uncertainty. The success of the bank’s interest rate setting strategy is measured through 3 indicators, namely the Operating Cost to Operating Income (BOPO) ratio, the Loan to Deposit Ratio (LDR) ratio and the difference between lending rates and deposit rates, namely the 1-month deposit rate.

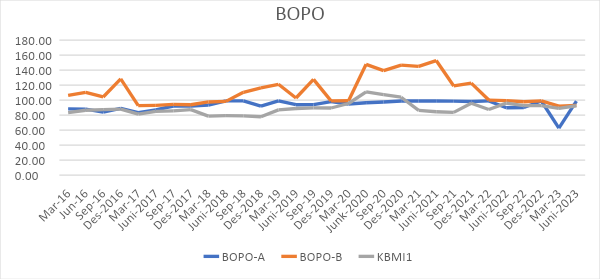

The correlation between BOPO and profitability

In general, BOPO in KBMI-1 increased from 77.85% in 2018 and 103.91% in 2020 and then gradually decreased to 95.91% (2021). For KBMI-1, the bank’s operating costs are relatively high, which is caused by various factors, such as labour costs, technology costs, and other operating costs. High operating costs can reduce bank profits. For bank A, BOPO is relatively maintained at an average of 98% from 2019 to 2022. In bank B, BOPO increased from 99.02% in 2019 to 146.06% in 2020 and then decreased to 99.04% in 2022.

The result of statistical test with 5% significance level, BOPO of KBMI-1 has significant value of 0.000 while bank A (significant value of 0.021) and bank B (significant value of 0.000). This proves that there is a significant correlation between BOPO and the level of bank profitability, where the implementation of the right strategy will have a positive impact on profitability. Interest rate setting strategies can affect a bank’s interest income. If a bank raises lending rates faster than deposit rates, it can increase interest income. This relationship can affect BOPO, as growth in interest income can help cover operating expenses.

The correlation between LDR and profitability

In general, LDR tends to be low for both bank A and bank B. For KBMI-1, LDR since 2018 is at 94.78%, rising to 98.20% in 2020 and then falling to 77.69% in 2022. Bank A’s LDR was at 51.96% (2018), 39.33% (2020) and 20.53% (2022), while bank B’s LDR was at 77.43% (2018), fell to 54.65% (2020) and rose again to 74.71% (2022). The statistical test results with a significance level of 5%, the LDR of bank KBMI-1 with a significant value of 0.024 while bank A with a significant value of 0.019 and bank B with a significant value of 0.001. This indicates a significant correlation between LDR and bank profitability, where the implementation of the right strategy will have a positive impact on profitability.

A high LDR can cause liquidity problems during economic downturns, while a low LDR indicates underutilisation of funds. Maintaining an optimal LDR by achieving a balance between loan growth and deposit growth is essential to maximise profitability and manage risk effectively. Furthermore, the relationship between LDR and the difference between lending rates and 1-month deposit rates can be reflected in the bank’s risk management strategy and interest rate policy. If the LDR is high, it means that the bank uses more customer funds to provide credit. In this situation, the interest rate differential between loans and deposits can be a significant factor in determining the bank’s profit margin.

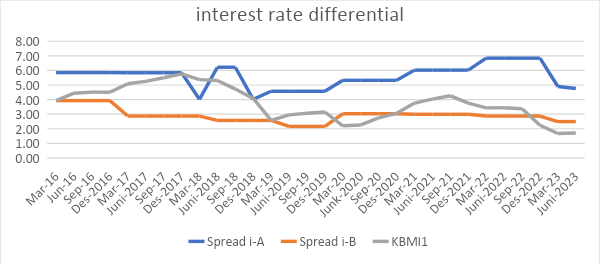

The correlation between loan interest rate differential and deposit interest rate on profitability

Based on the data, the difference between the lending rate and the 1-month deposit interest rate shows that bank A earns a larger margin from each loan it disbursed. This is because bank A’s average interest rate differential of 5.6% is greater than bank B which averages only 2.91% and even higher than KBMI-1 with an average of 3.74%. Bank A has a strategy to get a bigger profit from each loan it disburses. This can be seen from the difference in interest rates that are higher than bank B. In 2020 bank A obtained an increased income, which amounted to IDR 292.89 billion compared to the 2019 acquisition which reached IDR 222.81 billion. This increase was generally due to the recovery of loans that had been written off in previous periods. Related to interest rate differentials, Bank A’s net interest income in 2020 was IDR 47.35 billion compared to IDR 347.2 billion in 2019. This is due to the decrease in LDR which is in line with the bank’s policy to maintain liquidity by increasing the portion of deposits that have a higher interest rate and decreasing loans to maintain credit quality. The statistical test results with a significance level of 5% in KBMI-1 show that the significant value of the difference between loan interest rates and 1-month deposit interest rates is 0.000, while bank A with a significant value of 0.000 and bank B with a significant value of 0.001. This proves that there is a significant correlation between the interest rate setting strategy and the level of bank profitability, where the implementation of the right strategy will have a positive impact on profitability.

Conclusion

Based on the above discussion of KBMI-1 in the pandemic era, it can be concluded:

1. There is no significant correlation between the level of capital adequacy (CAR) and credit management strategy (NPL) with the level of bank profitability.

2. There is a significant correlation between interest rate setting strategy (BOPO, LDR and the difference between lending rate and deposit rate) with the level of bank profitability.

3. The government’s restructuring programme in 2020 succeeded in controlling the potential incidence of bad debts due to the pandemic. This policy can keep NPLs from soaring and banks can improve the condition of customers who are still able to survive and return to normal operations.

4. OJK’s policy to adjust the minimum core capital requirement for KBMI-1 had a positive impact so that the bank’s CAR did not decline.

5. Several policies in KBMI-1 banks, namely in bank A and bank B, to improve risk management, increase efficiency and the commitment of bank owners to place their funds in their respective banks have resulted in the capital adequacy requirement as stipulated by OJK, which is Rp 3 trillion by the end of 2022.

Recommendations

1. KBMI-1 is expected to play a greater role in supporting the economy:

- With the release of credit restructuring provisions, KBMI-1 needs to improve asset quality by maintaining the ratio of non-performing loans (NPLs) through improving the quality of credit analysis and conducting more effective collections.

- Managing sound risk management amidst the challenges of 2024, namely political issues, money laundering and intense competition for banking products.

2. OJK is expected to:

- Continue to encourage the implementation of adequate risk management for individual debtors and debtor portfolios, both sectoraly and by debtor business category (corporate, commercial and MSME). Banks (especially KBMI-1) that have been prioritizing the corporate business sector to pursue profits (from the difference in interest rates on loans and funds) should be encouraged to gradually increase their loan portfolio to MSMEs

- Increasing the efficiency of digital transactions in terms of cost, security and ultimately can encourage increasing the financial inclusion of people who were previously unbanked to have better access to banking.

3. Bank Indonesia needs to carry out several policies, such as:

- Periodic Monitoring and Evaluation of the effectiveness of the PLM policy in increasing lending by banks. By monitoring developments continuously, BI can identify potential improvements or adjustments needed.

- Collaboration with related parties. It is important for BI to work closely with OJK and other relevant parties, including banks and other financial institutions, in managing liquidity. Through dialogue and cooperation, BI can understand the needs and challenges faced by the banking sector.

Leave a Reply